Authorising a €30,000 international transfer to a factory in Shenzhen you have never physically visited requires a significant leap of faith. For many Irish businesses, the moment they hit "send" on their AIB or Bank of Ireland portal is the most anxious part of importing from China.

That anxiety is justified, but usually for the wrong reasons. The primary risk when paying Chinese suppliers is not the factory taking your money and vanishing. Legitimate factories want repeat business, not a one-off theft. The real risks are third-party invoice interception (where you pay a scammer instead of the factory), poorly structured payment terms that destroy your negotiating leverage, and the staggering hidden currency exchange margins that traditional Irish banks take on USD or RMB transfers.

This guide breaks down exactly how to structure your payment terms safely, how to verify supplier bank details, and how to transfer funds from Ireland to China without sacrificing 3 percent of your margin to FX spreads.

Payment Terms: Why 30/70 is the Gold Standard

In China sourcing, he who holds the money holds the leverage. Once you pay 100 percent upfront, your ability to negotiate rework, demand quality corrections, or enforce delivery timelines drops to zero.

The standard, universally accepted payment structure for OEM and ODM production in China is "30/70 TT", a 30 per cent deposit before production begins, and the remaining 70 per cent balance paid only after the goods have passed pre-shipment inspection but before they are loaded onto the vessel.

The 30 per cent deposit serves a specific commercial purpose for the factory: it covers the cost of raw materials and specifically confirms the order. The 70 per cent balance is your insurance policy. If the pre-shipment inspection reveals that the product fails CE compliance, the colour matches poorly, or the dimensions are wrong, the factory will fix the issue because they need the final 70 per cent of their money. If you paid 100 per cent upfront, fixing the problem is a cost they are highly incentivised to avoid.

Never agree to 100 per cent upfront on a production order. Some factories will push for 50/50, which is occasionally acceptable for custom-tooled products where the raw material input cost is exceptionally high. However, 30/70 remains the target. If a factory insists on 100 per cent upfront for a standard €20,000 order, you should immediately question their cash flow stability or their legitimacy.

The Invoice Interception Scam (Business Email Compromise)

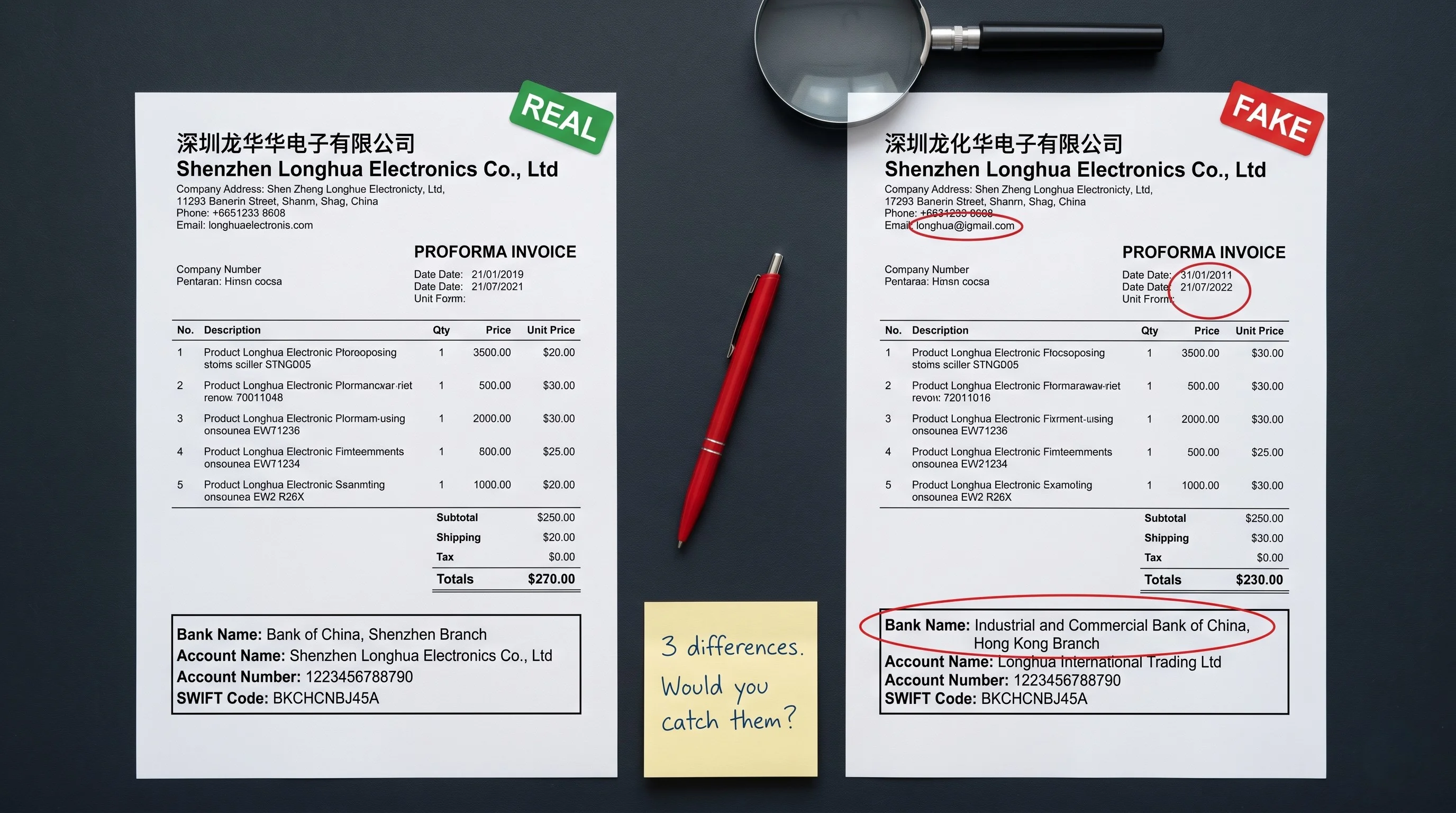

This is the single most common way Irish importers lose money in China. It is not perpetrated by the factory. It is perpetrated by hackers who have compromised the email account of either the factory's sales rep or your own business.

The scam works like this: You negotiate an order via email. The supplier sends a proforma invoice. Then, just before you make payment, you receive another email from the same supplier, perhaps from the exact same email address, or one off by a single letter. The email states: "We are currently updating our company bank accounts for the annual tax audit. Please send the payment to this alternative account in Hong Kong."

You update the beneficiary details, authorise the transfer at your bank, and the money clears. Two weeks later, the real factory emails asking where the deposit is. Your money is gone, sitting in a burner account in Hong Kong or Singapore, and the factory never received it.

Preventing this requires a hard, inflexible rule: Never accept a change of bank details via email.

If a supplier changes their bank details, you must verify it through a secondary channel independent of email. Call the factory directly using the phone number on their official website (not the number in the suspicious email signature). Alternatively, insist that the factory manager holds up the stamped bank details document on a live WeChat video call. No legitimate Chinese business operates without WeChat. If they claim a "tax audit" prevents them using their standard account, refuse to pay until the standard account is available.

T/T (Telegraphic Transfer) vs Trade Assurance

There are three primary ways to send money to China: Telegraphic Transfer (T/T), Alibaba Trade Assurance, and Letters of Credit (L/C).

Telegraphic Transfer (T/T): This is an international wire transfer via the SWIFT network. It is the cheapest, most standard method for B2B transactions. The funds move directly from your bank to the supplier's bank. However, T/T offers zero buyer protection. Once the money hits the supplier's account, it cannot be recalled. You only use T/T when you have verified the factory and trust the relationship.

Alibaba Trade Assurance: Think of this as an escrow service. You pay via credit card, Apple Pay, or wire transfer into Alibaba's holding account. Alibaba only releases the funds to the supplier once specific conditions (like shipping dates or inspection thresholds) are met. It provides excellent peace of mind for first-time buyers on smaller orders.

The downside of Trade Assurance is the cost and the dispute reality. It adds approximately 2 to 3 per cent to your transaction in processing fees. More importantly, if a dispute arises, Alibaba arbitrates. You must prove the goods are defective based strictly on the criteria defined in the digital purchase contract. If your contract was vague about "acceptable colour variation", Alibaba will likely release the money to the supplier. Trade Assurance is useful, but it does not replace the need for pre-shipment inspection.

Letter of Credit (L/C): An L/C is a financial instrument where your Irish bank guarantees payment to the Chinese supplier's bank, provided the supplier produces highly specific shipping and compliance documents. The banks manage the risk.

L/Cs are bulletproof security, but they are expensive, administratively exhausting, and generally ignored by Chinese factories for orders under $100,000. For an Irish SME importing €30,000 of goods, the bank fees and setup time make an L/C economically unviable. Stick to 30/70 T/T with rigid pre-shipment inspections.

The Hidden Cost of High Street Banks

Chinese factories typically price their goods in US Dollars (USD), though some are shifting towards offshore Chinese Yuan (CNH). As an Irish business, your capital is in Euros (EUR).

When you use a traditional Irish clearing bank (such as AIB or Bank of Ireland) to pay a $50,000 invoice, the bank charges you a flat SWIFT fee of perhaps €15 to €25. That is not the cost. The actual cost is hidden in the exchange rate spread.

Traditional banks typically apply a margin of 2 to 3 per cent on the interbank exchange rate. On a $50,000 payment, the bank is quietly keeping €1,000 to €1,500 by giving you a poor conversion rate. Over a year of quarterly shipments, that is €4,000 to €6,000 stripped directly from your net profit margin.

The solution is to use dedicated business FX providers. Platforms like TransferMate (an Irish unicorn), Revolut Business, Fire, or Monex Europe bypass the high street retail margins. They offer near-interbank exchange rates and charge transparent, fraction-of-a-percent fees. Opening a multi-currency business account with a fintech provider is the highest-ROI administrative task an Irish importer can execute.

Verifying Bank Details: Red Flags to Watch For

When a Chinese supplier sends you a proforma invoice with bank details, you must perform due diligence before authorising the SWIFT transfer. Look for the following alignment:

1. Does the beneficiary name exactly match the factory's registered name? If the verified factory is "Shenzhen Xinlong Manufacturing Co., Ltd", the bank beneficiary must be exactly that. If the beneficiary is "Xinlong Enterprises Limited" based in Hong Kong, you are paying a different legal entity. Often this is just the factory using a Hong Kong offshore account for tax efficiency, but you must ask the factory to officially confirm the relationship between the mainland manufacturing entity and the Hong Kong billing entity on stamped company letterhead.

2. Personal accounts: Never, under any circumstances, wire business funds to a personal bank account (e.g., standard names like "Wang Wei" or "Li Na"). Legitimate B2B manufacturing transactions occur between corporate entities. Paying a personal account voids any legal protection, violates Irish accounting norms, and is a hallmark of a scam.

3. The Company Chop: In China, a company signature means less than the official company stamp (the "chop"). The chop is a registered red ink seal that binds the company legally. Ensure the proforma invoice you are paying against is stamped with the official red corporate chop, and ensure the characters on the chop match the registered business name.

Conclusion

Managing payments to China safely is an operational discipline. It relies on strict internal protocols, not luck.

For your next invoice, verify the bank details on a video call. Pay 30 per cent upfront, demand a pre-shipment inspection, and only release the 70 per cent balance when the inspection report is passed. And route your EUR to USD conversion through an FX specialist to claw back your margin.

If you're unsure about stepping into the complexities of supplier payments and verified inspections, paying a sourcing agent is the safest route. Your agent verifies the factory, signs domestic legal contracts in Mandarin, and acts as your on-the-ground risk manager. If you need help managing sourcing compliance from Ireland, contact Ériu Sourcing.

Frequently asked questions

What is the safest way to pay a Chinese supplier?

For new relationships on orders under €10,000, Alibaba Trade Assurance provides escrow protection. For larger, verified B2B orders, Telegraphic Transfer (T/T) is standard, but safety comes from the payment structure: strictly 30% deposit upfront, 70% balance paid only after a passed pre-shipment inspection.

Should I use my Irish bank account to wire money to China?

No. Traditional Irish banks apply a 2-3% invisible markup on the EUR-to-USD exchange rate, which costs thousands on volume orders. Use a dedicated corporate FX specialist like TransferMate, Revolut Business, or Fire to get interbank rates.

The supplier changed their bank details to a Hong Kong account, is this normal?

It is common for mainland Chinese factories to use offshore Hong Kong accounts for USD receipt and tax efficiency. However, it is also the primary mechanism for invoice interception scams. Never accept a bank change via email. Verify the change over a secondary channel, such as a WeChat live video call with the factory manager.